.svg)

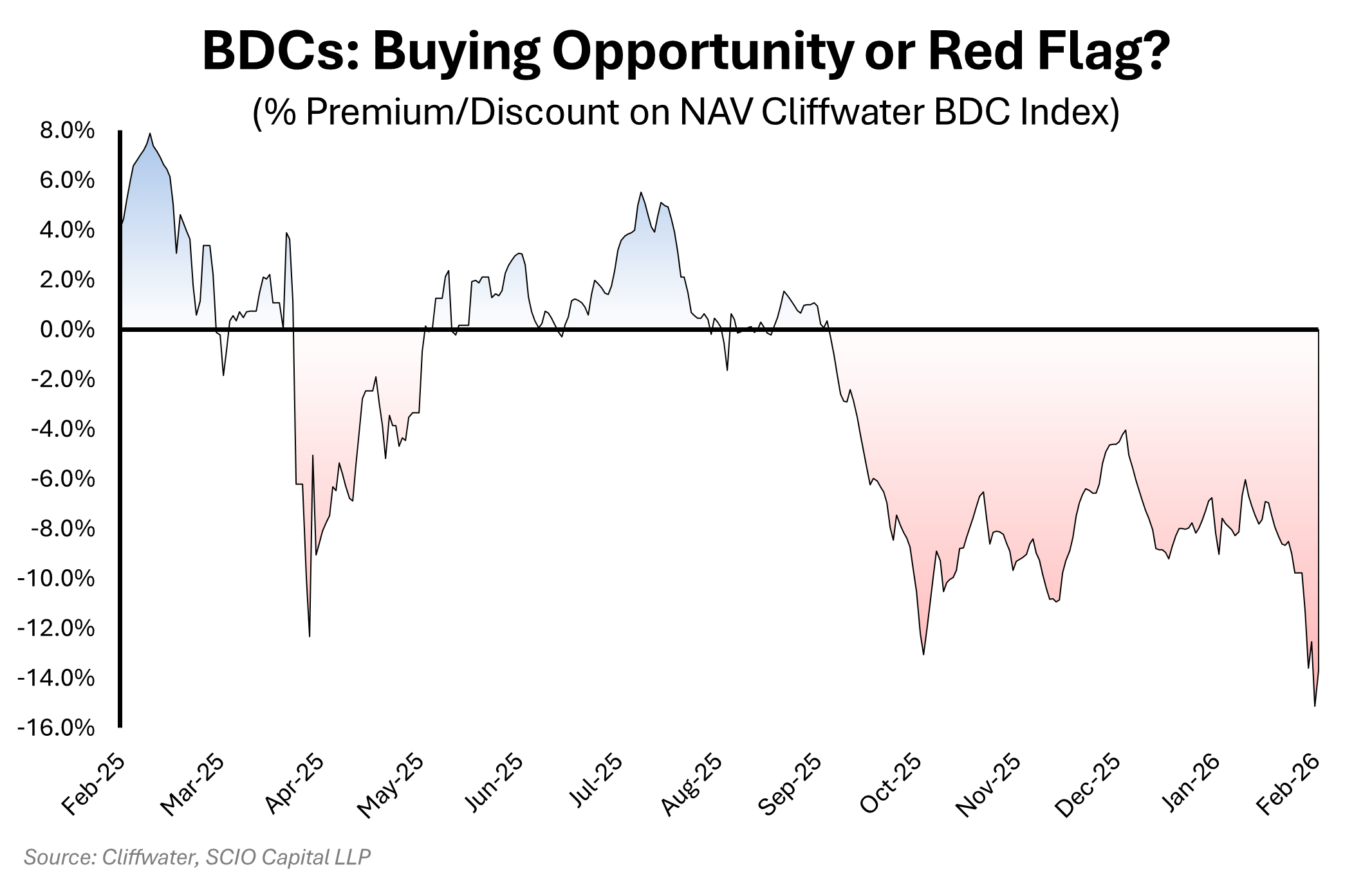

At a 13.7% discount to NAV, are BDCs a screaming buy?

A BUYING OPPORTUNITY?

This level of discount has been breached three times since 2020: during Covid, and twice more as the Fed aggressively raised rates in 2022. Investors who bought the BDC Index at those points were rewarded with 12-month gains of 114%, 14%, and 29% respectively... sizable returns for a credit product.

But before rushing out to buy, let’s take a step back and ask what’s actually driving the discount.

BDC Primer

A Business Development Company (BDC) is a closed-end, leveraged, publicly traded investment company that primarily lends to (and sometimes takes equity stakes in) small- to mid-sized private businesses. Conceptually, BDCs are a great idea: they offer a liquid, tradable way to access inherently illiquid private-credit assets.

The catch is that, in periods of elevated market stress, BDCs have historically traded meaningfully below NAV (i.e., below the estimate of their underlying portfolio value). In other words, they provide liquidity, but during panics that liquidity typically comes at a steep cost.

During Covid and 2022, that discount made intuitive sense: markets sold off aggressively and the VIX Index (a common gauge of equity-market volatility) spiked well above historical averages.

Today, the opposite is true. The VIX is below its longer-run averages.

WHAT'S DRIVING TODAY'S DISCOUNT?

So, if market volatility isn’t driving the current discount, what is?

We believe it’s credit fundamentals and, more specifically, confidence in marks.

Many BDCs have been active lenders to sectors that have come under pressure in recent years, notably e-commerce aggregators and certain software/business-services models. The result has been widely publicised portfolio write-downs. These businesses also tend to have limited tangible collateral, which can translate into weaker recoveries in default than in more asset-heavy industries.

Unlike prior episodes, the market may now be signalling scepticism about where some of these assets are currently marked and, by extension, how much cushion might still be in NAVs if credit conditions deteriorate further.

BDCs might be a buying opportunity at today’s levels but the key question isn’t simply “How wide is the discount?”, it’s “How reliable is the NAV?”

Only time will tell.

.png)

.svg)